3 High Growth Dividend Stocks To Buy Now

7 min readPaul Morigi/Getty Images Entertainment

It is better to be approximately right than precisely wrong. – Warren Buffett

Written by Sam Kovacs

Introduction

I haven’t proven anything. Yet.

When I claimed that the S&P 500 (SPY) had likely bottomed at 3,930 a couple of weeks ago, I got roasted, because the daily chart dipped another 30 points before bouncing.

This is a good time to ask oneself again: would you rather be roughly right, or precisely wrong?

Many times, I’ve suggested that the goal isn’t to pick the exact bottom or the exact top for any stock, but close enough to the top, and close enough to the bottom.

Even just buying closer to the bottom and closer to the top will be sufficient to best the market, but people don’t get that.

The human desire to “get one up” on strangers over the internet is astounding. If this is the game that some of our readers want to play, we’ll happily partake.

One such reader once challenged us to beat his suggested basket of tech stocks with the basket of boring dividend stocks we suggested in December 2020. So I tracked the portfolios. Ours outperformed by 79% so far. I send him a public reminder once every 6 months.

But this time around, the issue many readers have, is that they believe that the bull market is over, that everything is going to come down, and that it is game over.

Here are a few of the things which were said to me… (The joy of writing on the internet!)

a) 5000 yea, try fighting the Fed and let us know how that goes.

b) No thanks. It isn’t going higher in the short to medium term.

c) I read the title of this article and literally laughed out loud.

I could go on. There were a lot of them. I didn’t pick the meanest ones.

As stocks have now bounced, and the S&P 500 is looking towards a recovery, it seems ever likelier to me that the bottom is in.

Of course, this might not be it. But what I’m convinced of, is that the market is not done with the bull cycle:

- Too much liquidity still to boost consumption (over $2tn of pandemic stimulus still unspent);

- Too much excess cash in financial assets;

- Valuations at a reasonable level across the market (the S&P 500’s P/E of 21 is high but not excessively so);

- Too many people convinced this is the end.

The last point is of particular interest. I remember a similar sentiment happened in 2016 across market participants when the index dropped 15%. Investors would say that “7 years is the usual length of a cycle, it is the end of the cycle.” I’m not even sure what the fear “du jour” was. Something with China maybe.

That came and went, and the market pumped higher. Being scared is different than being right.

The trending news item on Seeking Alpha right now is “Conditions for global stock meltdown have been met” according to an indicator that mostly doesn’t work…

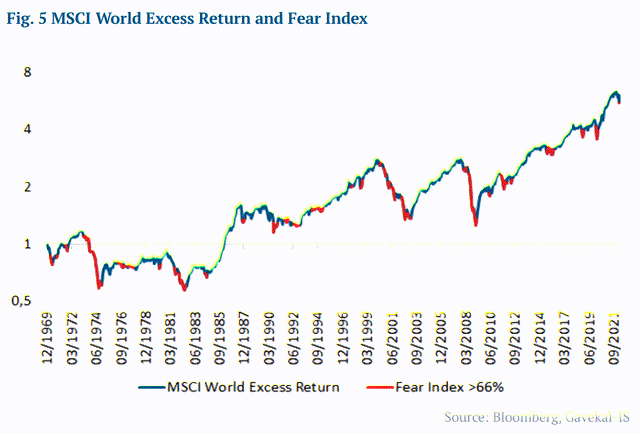

Gavekal’s Fear Diffusion Index, a measure of equity tail risks exhibited in 40 different markets, is now 70% on a scale of 0% to 100% (see chart at bottom).

But let’s look at the times when the index actually gave a “sell” signal.

It is highlighted in red below.

Bloomberg

As you can see, the Gavekal-IS is wrong at least as much as it is right. It would have told you to sell everything in 1981, 1990, then in 2010 and again in 2012, then in 2020.

Imagine how much poorer you would be if you used this as an indicator.

This is a great indication of how more money is lost in preparing for bear markets than in actual bear markets.

The gains you leave on the table could make or break your retirement dreams.

Now I do think that we are heading for total economic catastrophe, that the Fed will try and have its cake and eat it too by attempting to balancing the economy and inflation and ultimately fail.

But I do not think the market is over.

Especially not when so many, extremely high-quality dividend stocks, priced for disaster, are trading at such multiples.

Here are 3 amazing high-growth dividend buys which you should add to your portfolio today.

Lowe’s Companies, Inc. (LOW)

Dividend investors should strive to buy stocks when the combination of dividend yield and dividend growth potential is attractive.

This can sound vague, but we have it down very scientifically.

It’s not more than arithmetic.

We also use historical ranges of yield to determine when a stock is under or overvalued.

There is a peculiar set-up which often leads to attractive entry points.

This happens when a stock increases its dividend by an unusually high amount AND the stock price corrects significantly.

This can happen because dividends are not a short-term driver of price, but a long-term driver.

In the short term, the market is a voting machine, in a long term a weighing machine, and this is a perfect example of this.

In the past 6 months, LOW has dropped 30% in price AND increased its dividend by 33%.

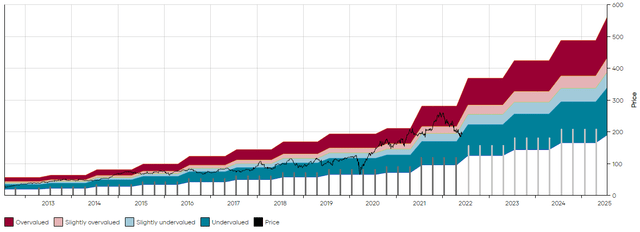

As you can see on the MAD Chart below (click here to learn more about MAD Charts), it is now historically undervalued, and quite significantly so.

Dividend Freedom Tribe: LOW MAD Chart

In the past 10 years, it has yielded more than this in less than 20% of trading days.

Given LOW’s very low FCF payout ratio of 35%, its history of delivering super-high growth from the topline which translates into earnings, cash flow, and dividends, it is very likely that we will continue to see LOW grow at double digits.

With its current yield of 2.14%, we believe it is an amazing high growth dividend buy today.

Based on our “required dividend growth” metric which calculates how much the dividend needs to grow for LOW to return 8% per year on the original investment, a decade from now, assuming dividend reinvestment, LOW needs to grow the dividend by 12%.

I believe this is extremely likely as the professional services segment continues to grow and management continues to deliver on its history of creating shareholder value.

LOW is a buy.

Amgen Inc. (AMGN)

In the listicles that I write, I like to give ideas in diverse sectors. I understand that some investors will be curious as to why we’re suggesting a consumer discretionary stock in the face of high inflation. This is reasonable, although we believe that the highest quality stocks should be bought when they are well priced, regardless of the macro, as this will work out for patient investors.

Which is why I’ll offer a stock in a much more defensive sector: Healthcare.

AMGN hit a rough patch during the past couple of years, with multiple setbacks from clinical trials.

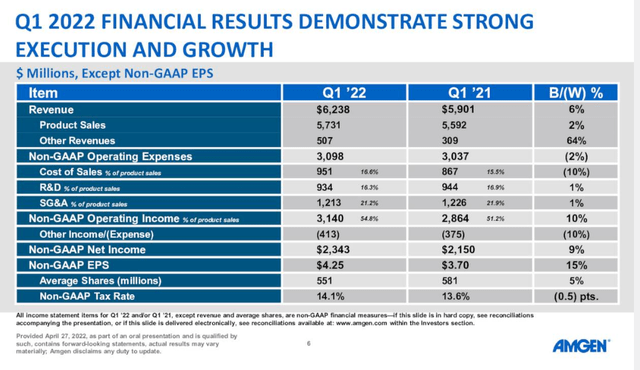

But this year, in Q1, revenue and earnings picked up again, which has fueled a revival in stock price activity after it hit its low.

AMGN Earnings Presentation

While we averaged the position down to a cost basis of $200, we believe AMGN is a great buy up until $260.

The stock has a strong history of dividend growth, although the 5-year CAGR of 11% is significantly lower than the 10-year CAGR of 18%.

Nonetheless, it currently yields 3.13%, which is historically very undervalued for the stock, and means it only requires 7.5% to 9% dividend growth to be a good dividend investment.

Dividend Freedom Tribe: AMGN MAD Chart

I believe that AMGN can likely continue to grow in the 8% to 10% range.

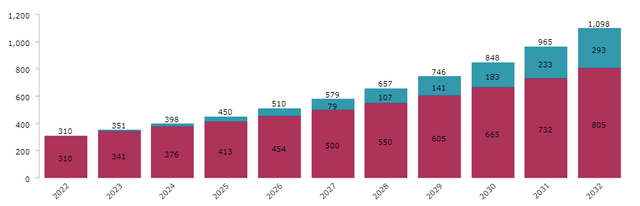

10% growth would provide a steady stream of income. Let’s simulate annual income assuming 10% growth for 10 years, annual dividend reinvestment, and a $10K initial investment.

Dividend Freedom Tribe: AMGN Dividend Simulation

In Year 10, an investor could expect $1,098 in income from their investment or an 11% yield on the original investment.

One of the key components of our strategy is to buy stocks which will be rewarding investments even if we never sell.

We do sell when stocks become overvalued, but we buy them at prices so good, that the income will take care of us regardless of what happens.

This is extremely desirable when you are uncertain of what will happen to the markets.

Even if I turn out to be wrong regarding market direction, which let’s not kid ourselves could happen (20% chance thereabouts), then you’ll still do fine buying these stocks.

BlackRock, Inc. (BLK)

The final stock on the list is BlackRock. As the world has become obsessed with passive investing, actively investing in BlackRock has become an attractive proposition.

Like most stocks, the pendulum swings from over to undervalued and back.

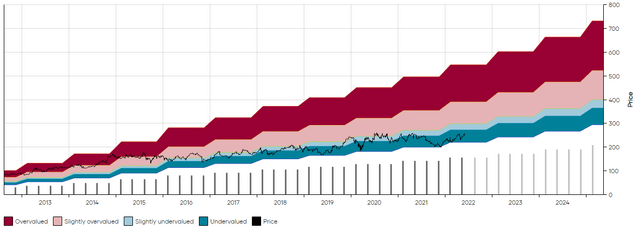

Dividend Freedom Tribe: BLK MAD Chart

Like many stocks that became overvalued in 2021, BLK took quite the beating this year.

But the combination of an 18% dividend hike and a 30% price drop has resulted in the stock being extremely undervalued.

Its current 2.8% yield requires dividend growth of 8.5% to 11%.

Over the past decade, BLK has established a history of growing at a CAGR of 12%. This accelerated to 14% over the past 5 years.

Given that index funds will remain a popular vehicle for a growing part of the population who don’t want to actively manage their investments, BLK will continue to do very well.

They have a huge moat which cannot be displaced at this point, which makes me extremely confident that investors can expect at least 10% growth for years to come.

BLK is also a great buy.

Conclusion

I believe the SPX is going to go above 5,000.

Whether you believe that or not doesn’t really matter. If this comes to pass, these stocks will likely do very well because they have growth which outpaces inflation, have unquestionable moats, and are attractively priced.

They are all great buys.